Accredited investor: a person or a legal entity who is allowed to participate in investments not registered with the U.S. Securities and Exchange Commission. An individual accredited investor is anyone who either earned income of more than $200,000 (or $300,000 together with a spouse) in each of the last two years and reasonably expects to earn the same for the current year, or has a net worth over $1 million, either individually or together with a spouse (excluding the value of a primary residence). (NerdWallet.com)

Analysis paralysis: a situation in which a person is unable to make an investment decision because they overthink and overanalyze the data. This is a common ailment that plagues newbie real estate investors. (Medium.com)

Average annual return: a rate of return metric that is calculated by taking the total profit received and dividing it by the original amount invested and then dividing that by the number of years an investment was held.

This is not to be confused with “annualized total return”, which is the geometric average amount of money earned by an investment each year if the annual return was compounded. (Investopedia.com)

Bad debt: in real estate, it is income that is deemed uncollectible from tenants that includes unpaid rent, late fees, pet fees, etc.

Blind pool fund (or private placement real estate fund): a direct participation program or limited partnership that lacks a stated investment goal for the funds that are raised from investors. In a blind pool, money is raised from investors, usually based on the name recognition of a particular individual or firm. They are usually managed by a general partner who has broad discretion to make investments. A blind pool may have some broad stated goals, such as growth or income, or a focus on a specific industry or asset. (Investopedia.com)

Break-even occupancy ratio: the sum of all operating expenses and debt service, divided by the total potential rental income. This tells you what percentage of the property must be leased in order to cover all expenses and debt service obligations. This ratio refers to the economic occupancy and not the physical occupancy. (PropertyMetrics.com)

Bridge loan: short-term commercial real estate loans that are used for the purchase of commercial properties when permanent financing is not an option. Their primary use is when a property needs significant renovation before it will qualify for permanent financing. (FitSmallBusiness.com)

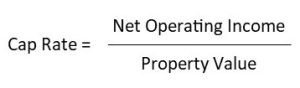

Cap (Capitalization) rate: the rate of return expected to be generated from the all-cash (i.e. no leverage) purchase of a property. It is calculated by taking the net operating income (NOI) and dividing it by the asset value. (CREPedia.com)

CapEx (Capital Expenditures): money used to add to or improve a property beyond common repairs and maintenance, such as replacing a roof or windows, paving a parking lot, or buying major appliances. (Fool.com)

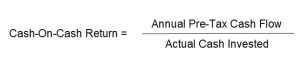

Cash-on-cash return: a percentage that measures the pre-tax cash flow relative to the money invested in an asset. It is calculated by taking the net operating income and dividing it by the total cash investment. (BiggerPockets.com)

CMBS loan: commercial mortgage-backed securities, or conduit loans, that are used to purchase commercial real estate buildings and are typically non-recourse and fully assumable. The minimum loan amounts are higher than for agency loans. (Fool.com)

Concessions: an incentive or discount given to a tenant by a landlord to make a lease more enticing. (CREPedia.com)

Cost segregation study: a tax strategy that allows real estate owners to utilize accelerated depreciation deductions to increase cash flow, and reduce the federal and state income taxes they pay on their rental income. (TheRealEstateCPA.com)

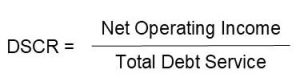

DCR (Debt Coverage Ratio) / DSCR (Debt Service Coverage Ratio): In the context of corporate finance, the debt-service coverage ratio (DSCR) is a measurement of a firm’s available cash flow to pay current debt obligations. In the context of personal finance, it is a ratio used by bank loan officers to determine income property loans. (Investopedia.com)

Depreciation: an important tool for rental property owners that allows them to deduct the costs from taxes of buying and improving a property over its useful life, and thus lowers their taxable income in the process. (Investopedia.com)

Due diligence: the use of reasonable care in an investigation of the relevant facts, assumptions, parties, conditions and subject matter pertinent to a transaction. In a real estate transaction, due diligence would include an investigation into the ability of the parties involved to conclude the transaction, a confirmation of the market and financial assumptions underwriting the property, an investigation into the condition of the subject property, and the fitness or regulatory restrictions applicable to the subject property’s intended use. (CREPedia.com)

Economic vacancy: the difference between the actual rental income and the gross potential rent of a property. This includes several other factors, such as tenants that have not paid rent, units that are occupied by a property manager or are otherwise “given” away, turnover periods between tenants, and rental incentives, such as a free month of rent or a percentage-based rental discount. (CommercialRealEstate.loans)

Effective Gross Income (EGI): the actual amount of income that a rental property is expected to generate. It is the total income expected from all operations of the rental property after an allowance is made for the revenue that is lost from vacancy or unpaid rents. (MashVisor.com)

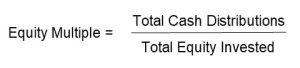

Equity multiple: the total cash distributions received from an investment, divided by the total equity invested. Essentially, it’s how much money an investor could make on their initial investment. An equity multiple less than 1.0x means you are getting back less cash than you invested. An equity multiple greater than 1.0x means you are getting back more cash than you invested. (Crowdstreet.com)

Executive summary: a syndication’s marketing packet discussing the particulars of a real estate investment. No two look the same but all will include an overview of investment including photos, detailed metrics and forecasted numbers, the business plan, and information on the management team.

Expense ratio: a measurement of the cost to operate a piece of property, compared to the income brought in by the property. It is calculated by dividing a property’s operating expense (minus depreciation) by its gross operating income. (Investopedia.com)